“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”- Peter Lynch, well-known investor

Market Shows Resiliency

Once again, the U.S. stock market proved to be remarkably resilient. During March 2022, the S&P 500 advanced just shy of 4%1 in the midst of a rather intimidating wall of worry that is loaded with items such as shifting Fed policy, sticky inflation at elevated levels, rising rates, some coronavirus surges overseas, the Russian military campaign in Ukraine, rising odds of changes in congressional leadership during the upcoming November midterm elections, and yes, rumblings in some pockets of the investor world that a recession might be around the corner sooner than we realize. After correcting by 13% and falling from a record high of 4,796 on Jan. 3, down to the most recent low of 4,170 on March 8, the S&P 500 has surged back to 4,531 as of April 1.2 This is not as impressive as the S&P 500’s extremely swift and robust recovery from the 35% swoon in the month of March 20203 inspired by the pandemic-related economic shutdown back then, but it clearly demonstrates the risk of trying to attempt to perfectly time the market on or around short-term and normal market corrections.

This can lead to seller’s remorse and significant whiplash as the market quickly bounces back from short-lived swoons caused by headline fears rather than hard data and metrics that we follow closely and that truly drive the market. Regardless of the validity of some of the wall of worry items mentioned above, the market was due for a pullback simply after an extremely fertile advance of 26% per year over the last three calendar years.4 We have messaged to clients from the beginning of the 2022 to expect a correction on the order of 15%-20% this year and not to freak out if this was to occur. The market usually sees one 10% correction and three 5% corrections each year based on history.5 In 2021, we had a max drawdown of 6%,6 so the abnormality has been the lack of volatility these past several years, not the volatility we have seen in the first quarter of 2022. The point is that yet again, at least for the time being, the smart move for investors is to do nothing. Assuming you are already balanced and properly diversified and that you are at your normal long term equity allocation prescribed for you, we continue to endorse a “stay put” portfolio approach at present. The growth versus value results in March are a great example of the importance of balance. So many experts have been suggesting that investors should swing whole heartedly to economically sensitive, value-oriented stocks and abandon growth altogether. We believe this is unwise. We see catalysts for both camps and think a blend of both is best in the midst of an ongoing rotation in leadership between these two types of stocks. This mindset paid off in March as growth stocks well outperformed value stocks after underperforming earlier in the year.7

Successful Investors Are Patient Investors

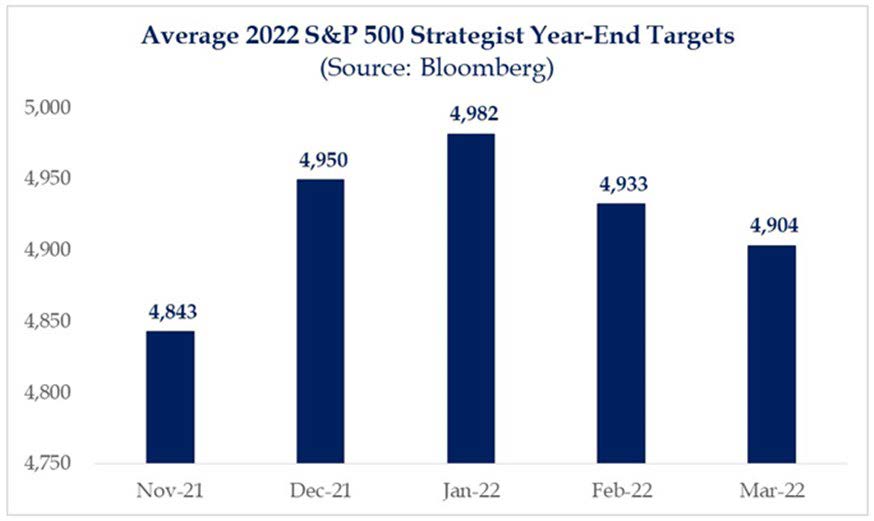

Bottom line, we absolutely agree with famous investor, Peter Lynch, that successful investors exude patience and poise in moments of heightened fear when emotions are riding high…when the facts and the data support doing so. We believe the economic data remains healthy and that valuation is reasonable. Despite this, investor sentiment is rather bearish at present. This is a rather nice cocktail when it comes to assessing the market backdrop. Holding fast to a contrarian, constructive stance is the right side of valor in our mind when the fundamentals, valuation levels, price trends and investor sentiment lineup as they do currently. We maintain our price target of 5,000 for the S&P 500 at year-end and do not see recession as a base case outlook. Our Chief Economist, Bill Greiner, places only 20% odds of recession in the near-term at present, as you’ll note in his commentaries. For perspective, please note that the average target for key investment strategists is 4,900, so we are not prophesizing something far above industry consensus this year.

That said, well-known strategists in our industry are exhibiting some fickle behavior this year that has caught our attention. Several set a price target for the S&P 500 at or around 5,000 going into the year, only to reduce their target in the middle of the quarter and then were moved to revise their target back up toward quarter-end. We find such revision-happy behavior confusing to clients and unactionable. And it can lead to wealth destruction. We will change our view when we find it warranted by the facts.

What About the Federal Reserve?

Along with inflation, this is one of the most frequently asked questions that we get and a wall of worry item worth discussing. We frame-up our view by pointing out the Fed has maintained a historically high level of accommodation via extremely low short-term rates for several years, most recently to pull us out of the economic shutdown that occurred during inception of the pandemic back in 2020. Yes, it is raising rates now, but only taking them back to normal levels of 2%-3% over the next couple of years and in line with what they expect to be equal to the level of the longer-term level of inflation in the future. In a historical context, this is far from restrictive Fed policy. It is nothing like the 6% Fed funds rate we saw back in the tech bubble days of 2000, for example. The Fed has said that it is shifting its primary objective of helping the economy to find the full employment marker to that of calming inflation. That makes sense to us now that we have indeed achieved full employment thresholds.8 The Fed gets the message that it needs to more seriously address the inflation levels it sees at present, but there is talk about moving us to only normal levels of rates, not to restrictively high levels that choke demand and the economy. It is not until we see that it is signaling that it is targeting restrictive levels of interest rates that we will turn negative on the monetary policy front. Interestingly, the stock market has tended to generate healthy returns in the early innings of Federal Reserve rate hikes, and the Fed has demonstrated an ability to hike rates and orchestrate a soft landing rather than a recession on at least three occasions in recent history…in 1965, 1984 and 1994. Further, there is good reason to expect inflation to calm if certain factors normalize or fall into place. This elevated level of price increases is not the result of the normal runaway demand strain…there are supply chain bottlenecks that will be solved if coronavirus continues to evolve from pandemic to endemic, and commodity shortages will heal swiftly should we get some good news on the Russia-Ukraine front. Stay tuned, but we think it is way too early to expect worst case outcomes on the Fed policy front.

The Yield Curve Is Inverting…the Yield Curve Is Inverting

We have heard this before. Specifically, we heard the “inversion” warning cry back in December of 2018, and it was sure to cause a recession. Not so…the faux recession never occurred, and the 31% return in the S&P 500 in 2019, after such warnings, surprised many of our peers. We remained very bullish and maintained a “buy-on-the-dip message” throughout this period, because the economic and earnings data remained robust as did the credit backdrop. In our view, the yield curve never truly inverted in a sustained way, and it was never confirmed by other key factors. We don’t predict, rather we watch for what the robust indicators, like the shape of the yield curve, actually do and then we act. It is true that each and every U.S. recession has been presaged by an inversion of the yield curve. But cause and effect is not as simple as it sounds in this statement. First, the range in the time lag between inversion and recession is 12-18 months with an average lag time of 16 months,9 and the stock market has flourished many times during the lag period. So, selling at the inception of yield curve inversion can be a money- losing proposition. Patience can be rewarded even in the early goings after inversion.

Further, there are yield curve inversions, and then there are real yield curve inversions. You need to look at several yield curves to determine the signal and time matters as well. If one yield curve—such as the 2-year to the 10-year Treasury curve inverts, it needs to do so for more than an afternoon or one day to truly send a signal. Back in 2018, this curve inverted for a couple of days and then quickly un-inverted, so hence no real signal occurred…we must see sustained inversion for it to be a true leading indicator. Further it pays to see several curves invert to get confirmation. The two most watched are the 2-year to 10-Year Treasury mentioned above as well as the 3-month to 10-Year, which the Fed influences. Right now, because short-term Fed funds rates are so low, the 3-month to 10-Year is steep with a positive slope of almost 230 basis points10… it isn’t close to being inverted. Interestingly it is this latter curve that is included in the leading economic indicators. It’s best to get confirmation among both of these metrics.

U.S Treasury 2-Year and 10-Year Spread

U.S Treasury 3-Month and 10-Year Spread

Couple the lack of sustained inversion with the still very positive spread between the 3-month and the 10-Year Treasury, and the still tight credit spreads between corporates and treasuries in general, and we believe the signals are yellow-flag in nature and cautionary, not red-flag oriented.

Again, we will not predict the predictors. Only when they turn red do we shift our view. And historically, after this one has truly turned red, there is still time to make effective portfolio adjustments accordingly.

Risk of Recession

Bill Greiner, our chief economist, has discussed this in detail and has done a great job of regularly updating the investment team in regard to his research on this front. We embrace his view of 20% odds of recession. The reason his assessed probability of recession is still relatively low and comprises his least likely economic scenario is that none of the three primary recession signals are flashing red at this moment:

- The shape of the yield curve is concerning but only cautionary at present, as discussed above

- The Purchasing Managers Indices for Manufacturing and Service Companies are signaling healthy levels of activity and not close to recessionary levels of below 50.11

- The Leading Economic Indicators Index (LEI)—the annual percentage change in the LEI hovers close to the 0% level in advance of recessions; the current reading is a very healthy 7.6%.12

Bill currently expects GDP growth of 2.5%, and inflation to calm to the 4% level by year-end. This coupled with our expectations for 8%-10% earnings growth is supportive of mid- to high-, single-digit returns for U.S. stocks this year.

Wrap-up

A “stay put” approach is where we’re at in this environment. As a caveat, if you allowed your equity allocation to drift up to higher-than-normal levels because of such robust returns these last three years, make sure you have consulted with your wealth advisor and discussed rebalancing back to your long- term stock target out of respect for some rising risks in the market this year including war and geopolitics. Our base case remains a positive one, and our assessment of the odds of suffering from the dual risks of recession and a longer more painful bear market (versus simply experiencing a moderate deceleration in real GDP growth and an annoying yet short-term and normal correction) remains relatively low.

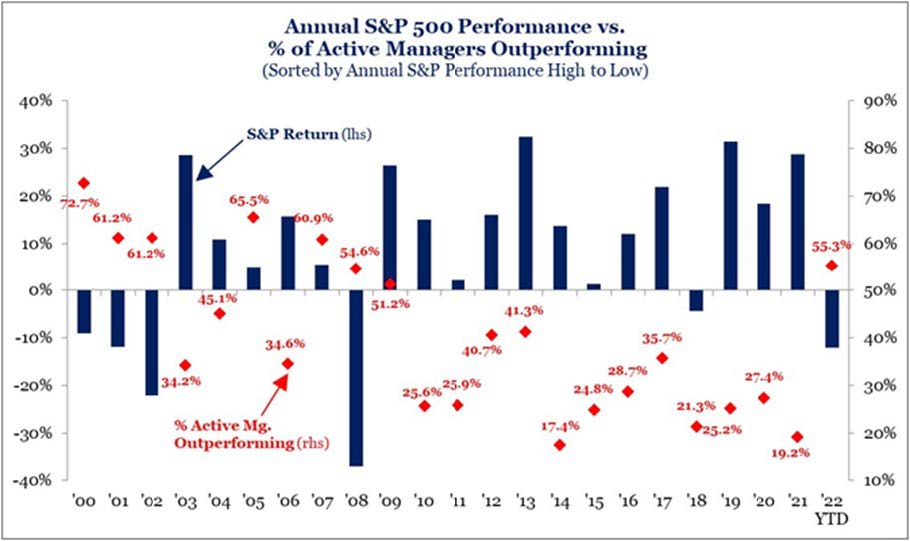

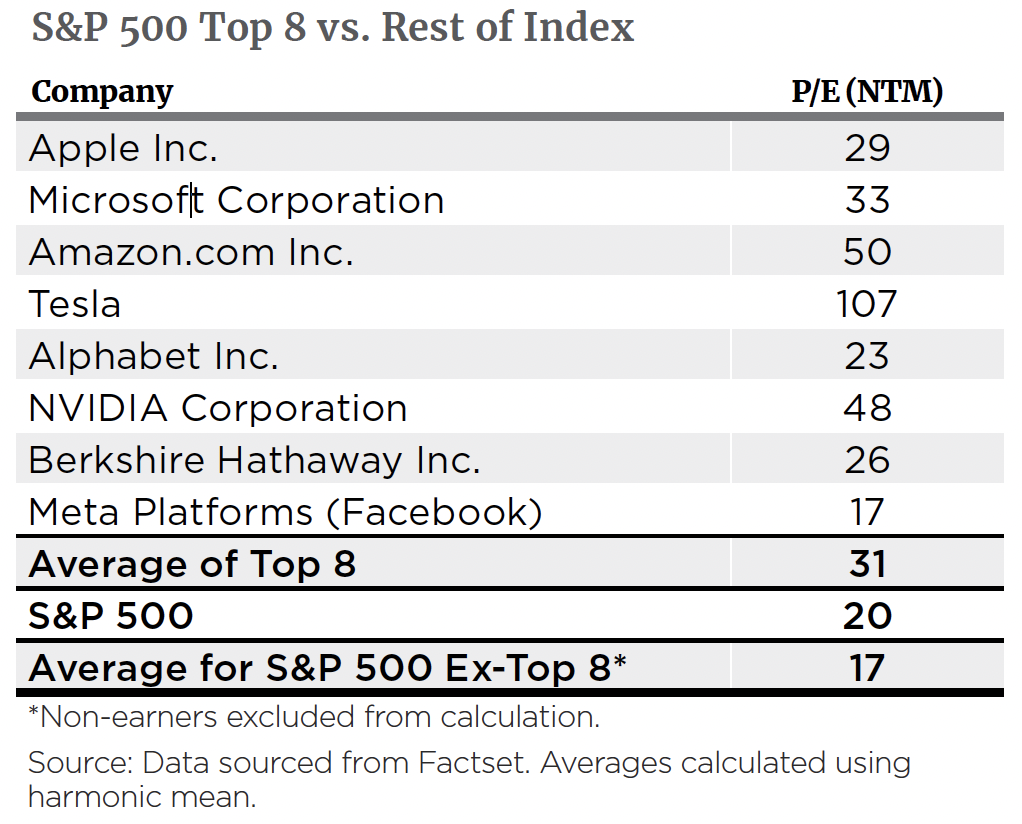

Finally, this could be an excellent time for active management…as the charts below illustrates, active equity managers tend to perform well when the Fed is hiking rates, and stock valuation amongst individual stocks is as disparate as it is today. In such periods, strength of balance sheet and the wide range in P/E levels create opportunities for specific stock selection. Passive management is most effective when abnormally low rates and extremely accommodative Fed policy lifts all boats; when this begins to unwind, what individual securities you own can matter to a much larger degree.

Thanks for your continued confidence and stay tuned!

Footnotes

1,2,3,4FactSet

5LPL Financial

6JP Morgan Guide to the markets

7FactSet

8Jerome Powell, March 21 Speech Transcript

9Strategas

10,11,12FactSet

The S&P 500 Index is a market-value weighted index provided by Standard & Poor’s and is comprised of 500 companies chosen for market size and industry group representation.

The impact of COVID-19, and other infectious illness outbreaks that may arise in the future, could adversely affect the economies of many nations or the entire global economy, individual issuers and capital markets in ways that cannot necessarily be foreseen. The duration of the COVID-19 outbreak and its effects cannot be determined with certainty.

This commentary is limited to the dissemination of general information pertaining to our investment advisory services and general economic market conditions. The views expressed are for commentary purposes only and do not take into account any individual personal, financial, or tax considerations. As such, the information contained herein is not intended to be personal legal, investment or tax advice or a solicitation to buy or sell any security or engage in a particular investment strategy. Nothing herein should be relied upon as such, and there is no guarantee that any claims made will come to pass. Any opinions and forecasts contained herein are based on information and sources of information deemed to be reliable, but we do not warrant the accuracy of the information that this opinion and forecast is based upon. You should note that the materials are provided “as is” without any express or implied warranties. Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. Past performance does not guarantee future results. Consult your financial professional before making any investment decision.

Investment advisory services provided through Mariner Platform Solutions, LLC (“MPS”). MPS is an investment adviser registered with the SEC, headquartered in Overland Park, Kansas. Registration of an investment advisor does not imply a certain level of skill or training. MPS is in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which MPS transacts business and maintains clients. MPS is either notice filed or qualifies for an exemption or exclusion from notice filing requirements in those states. Any subsequent, direct communication by MPS with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For additional information about MPS, including fees and services, please contact MPS or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you invest or send money.

Investment Adviser Representatives (“IARs”) are independent contractors of MPS and generally maintain or affiliate with a separate business entity through which they market their services. The separate business entity is not owned, controlled by or affiliated with MPS and is not registered with the SEC. Please refer to the disclosure statement of MPS for additional information.